In the management of any business institution, to be sustainable, the level of efficiency and effectiveness must be given attention. The Islamic commercial bank business in Indonesia should also do this. One of the main challenges of managing an Islamic bank is to find an efficient portfolio composition in Islamic commercial bank financing. If the bank manager misallocates the financing, it can be fatal. Because each type of financing has different characteristics. There are financing contracts that have high risk characteristics but also promise high returns, there are also types of financing contracts with small risks but the profits are also small.

To find a balance point in the composition of financing in Islamic banks in order to obtain an optimal level of profit but with a rational level of risk, an efficient portfolio theory was introduced by renowned financial expert, Markowitz, from America. This theory is a modern portfolio theory that is used to analyze the formation of a combination of composition from several investment instruments to form efficient portfolio combination points on the efficient frontier line. The measurement of efficient portfolio composition in this study uses the level of profit, standard deviation, variance-covariance, correlation coefficient and coefficient of variation of several investment instruments for the period of 2011-2015. The research method used is a quantitative method. This study uses the Markowitz portfolio model which is processed with Microsoft Excel software using the Solver application.

The first stage is the formation of an efficient portfolio composition is calculating the average value of profit / return, standard deviations, covariance values of all types of investment financing, then a combination of efficient portfolio can be formed using the Solver application with certain constraints. From the results of this calculation it can be concluded that the majority of ijarah financing has the smallest proportion compared to other financing, although ijarah financing returns on Islamic banks contribute the most. It happens because in this study the author uses Markowitz’s efficient portfolio theory, where the factors that become the object of research are only focused on risk and return while other factors are ignored.

Because the average return data of ijarah financing has quite extreme fluctuations, where the highest level and the lowest level numbers are widely gapped, then with a very wide range of results Markowitz portfolio theory calculation produced the highest risk followed by the highest average return compared to other financing. So in the formation of an efficient portfolio, ijarah financing must be reduced to the lowest proportion compared to other financing.

The optimal portfolio can be determined in two ways, by choosing a certain expected rate of return and then minimizing the risk, or determining a certain level of risk and then maximizing the expected return. Rational investors will choose this efficient portfolio because it is a portfolio formed by optimizing one of two dimensions, return on expectations or portfolio risk.

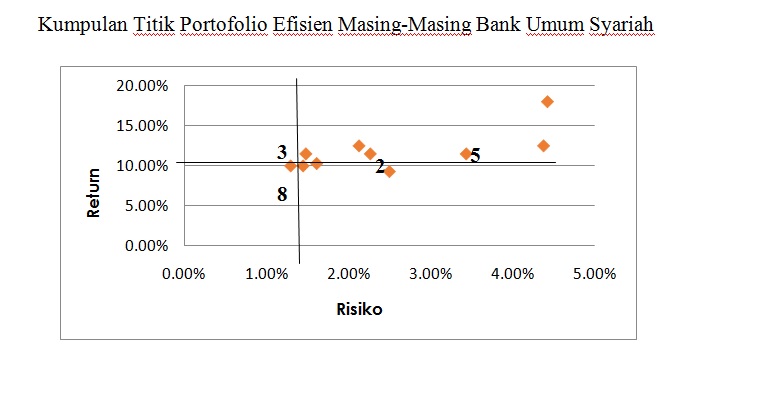

From the graph depicted above it can be seen that Bank Syariah Mandiri, which was shown in number 3, has the most efficient combination of portfolio proportions compared to other banks. Where at that point the relative risk is almost the same, but the expected return at number 3 is higher than the expected return at number 8. Same thing happened with points number 2 and 5, because with the same expected return, portfolio risk number 3 is smaller compared to portfolio risk numbers 2 and 5.

The results of this study showed that Bank Syariah Mandiri has the most efficient combination of portfolio proportions compared to other banks with an expected profit rate of 11.5%, a risk level of 1.48% and the lowest variation coefficient of 0.128 consisting of 92.82% mudharabah-musyarakah financing, 0% murabahah financing, 0.86% ijarah financing and 6.32% istishna financing.

Author: Dr. NISFUL LAILA SE., M.Com.

To read more about this paper, you can see this article at: